Text Size

Menu

close

Ensuring that the Fund can continue to pay benefits over the long-term, even during challenging times, is of primary importance to the Pension Board, clients and wider stakeholders. Through careful management of its solvency since its inception, the Fund is financially strong. Participants and beneficiaries can be assured that their UNJSPF benefits are secure.

The Fund’s ability to pay benefits is monitored through regular actuarial valuations (every two years) and asset liability management (ALM) studies (every four years). These studies consider alternative scenarios of increasing and decreasing numbers of participants, and high and low investment returns. This allows the Board to assess the risk associated with these and other variables.

Even in the stressed hypothetical situation of all participants separating immediately, recent actuarial valuations have shown that the Fund would be able to fulfill its obligations to pay client benefits.

The following sections provide further detail on the Fund’s actuarial valuations and ALM studies as part of its ongoing solvency monitoring.

The actuarial valuation considers the Fund from different perspectives, including:

With liabilities extending over an average of 40 years into the future, the actuarial valuation takes a long-term view of the Fund’s assets. Short-term market fluctuations in assets are smoothed. This minimizes the risk of the long-term assessment being distorted by short-term capital market movements (both up and down) that should not impact the Fund’s ability to meet its obligations.

Recent actuarial valuation results

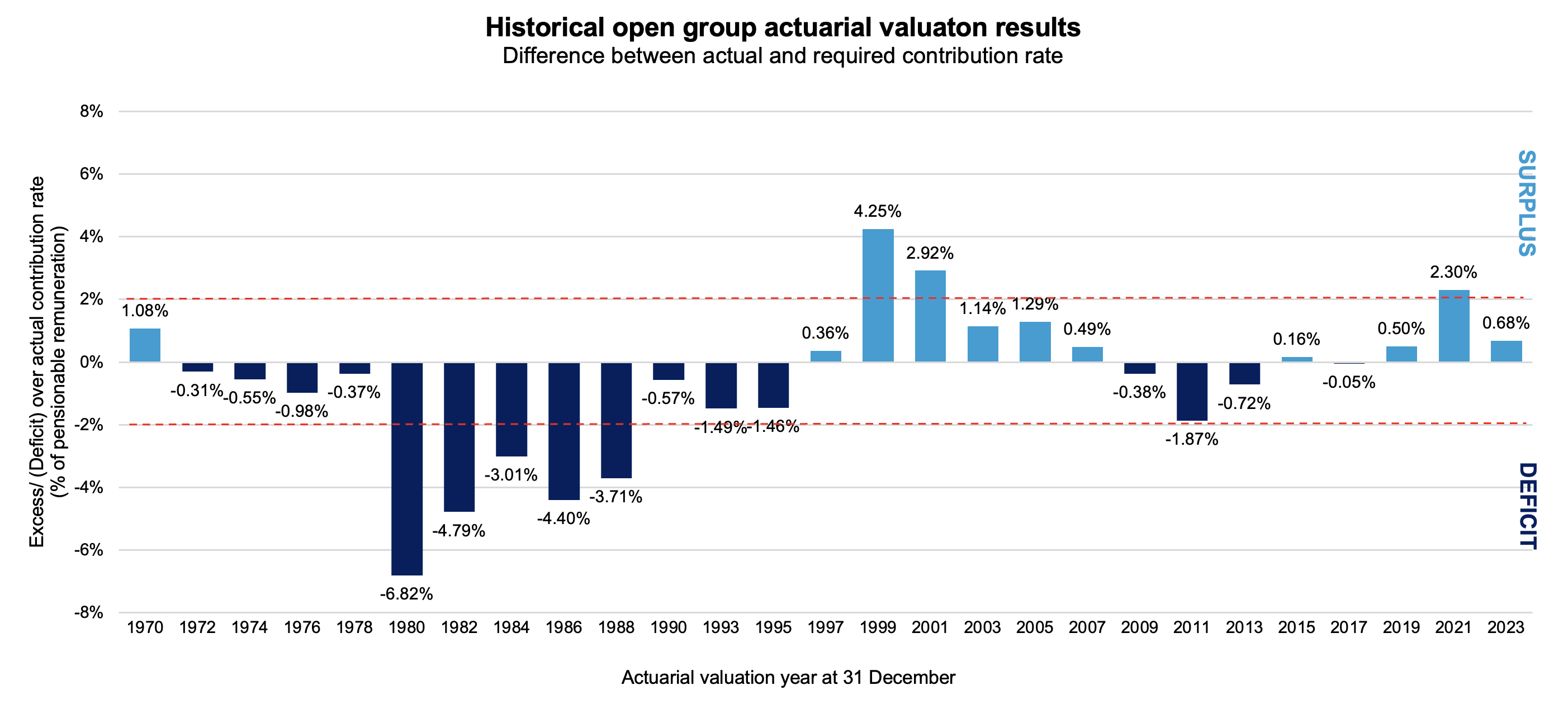

Open group valuation: The 2023 actuarial valuation resulted in a required contribution rate of 23.02% of pensionable remuneration to fund the pension plan adequately, which equated to an actuarial surplus of 0.68% of pensionable remuneration. The following graphic shows historical results and how the Fund has sought to maintain its surplus/deficit within +/- 2% around the current contribution rate of 23.7% of pensionable remuneration.

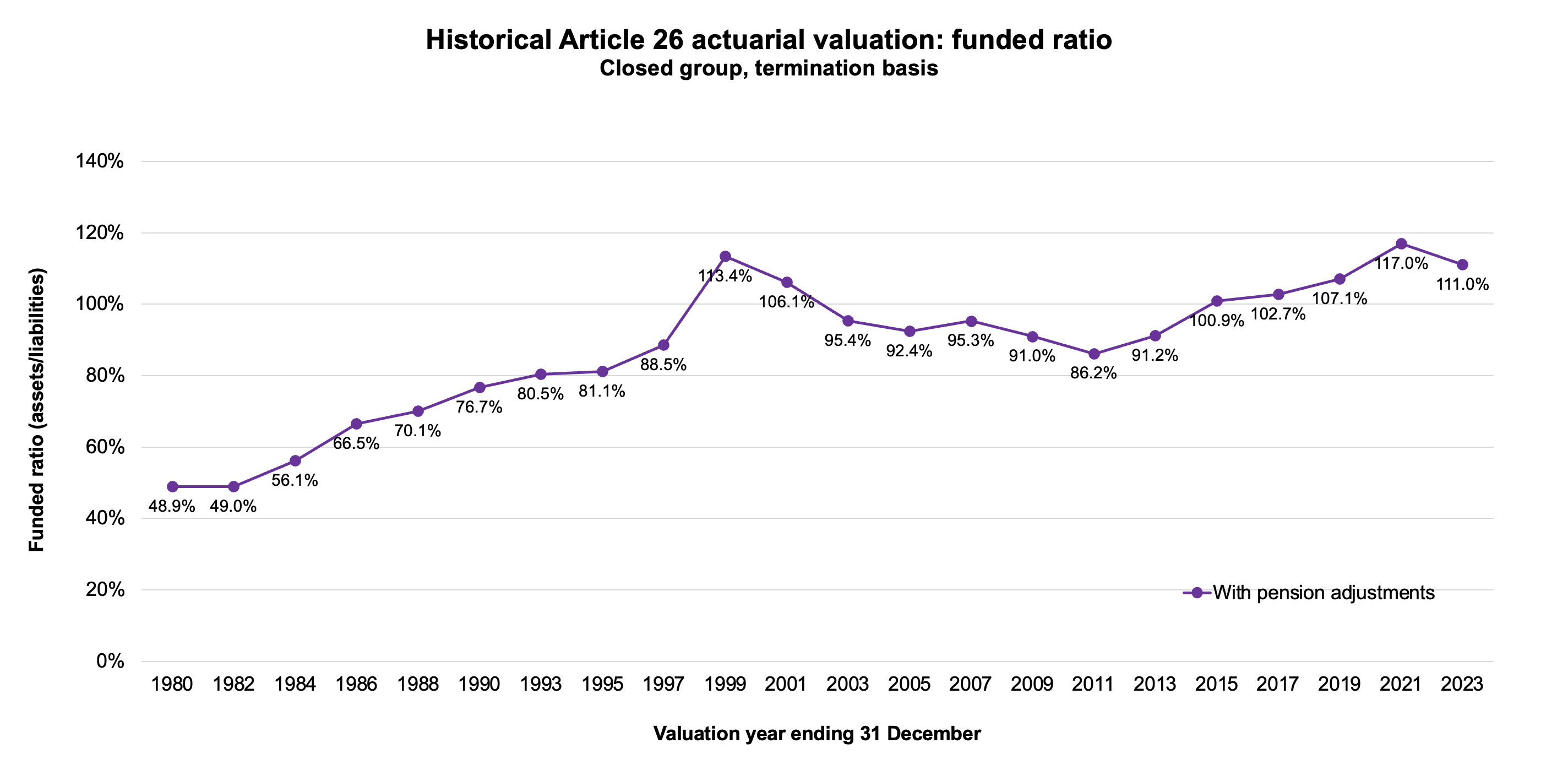

Closed group valuation: The 2023 valuation resulted in a closed book valuation of accrued benefit liabilities of US$83,151.2 million, as compared with an actuarial value of assets of US$92,322.9 million. This equates to a funded ratio of 111.0%, with the historical funded ratios summarized below. This means that if all participants were to separate immediately, the Fund should be able to comfortably pay all future expected benefits.

Every four years, the Fund conducts an ALM study using an expert, external consultancy firm. The study assesses the impact of key investment and solvency-related decisions on the long-term financial condition and performance of the Fund. A key objective of the study is to recommend strategic asset allocations that would improve the Fund’s long-term financial outlook.

The 2023 ALM study considered various scenarios for the future, including scenarios that incorporated climate risk. The Board noted that, under a baseline scenario with moderate growth and a suitable asset allocation, the Fund should still expect the current contribution rate to be adequate to sustain future benefits. The ALM study provides crucial insight for the Fund’s Office of Investment Management to develop its future strategic asset allocation, focusing on continued risk management to ensure long-term sustainability of the Fund.

All ALM studies are available here.

The Fund also maintains a Funding Policy, which is approved by the Pension Board. The purpose of the UNJSPF Funding Policy is to assist in ensuring that the Fund’s obligations to beneficiaries can be met over the long-term. The policy sets out the methods, processes and targets that are used to monitor the funding position and associated risks.

These studies and other actuarial matters in the Fund are supported by the Committee of Actuaries, comprising an international group of independent actuaries, with actuarial services provided by the Consulting Actuary, as set out in the Fund’s Regulations.