Text Size

Menu

close

Climate change will have a profound impact on pension plans worldwide. Whether through physical risks, technological innovations or governmental policies, climate change impacts the economy and the financial markets. This in turn affects the performance and sustainability of the pension plan.

To further integrate climate analysis over the short, medium and long term, the Fund’s Office of Investment Management (OIM) assessed the Fund’s exposure to climate risks across multiple scenarios in its Asset-Liability Management (ALM) study in 2023. With the expertise of Ortec Finance, global provider of technology and solutions for risk and return management for financial institutions, OIM integrates climate risk in its modelling to understand risks and opportunities arising from climate change and make informed asset and liability decisions.

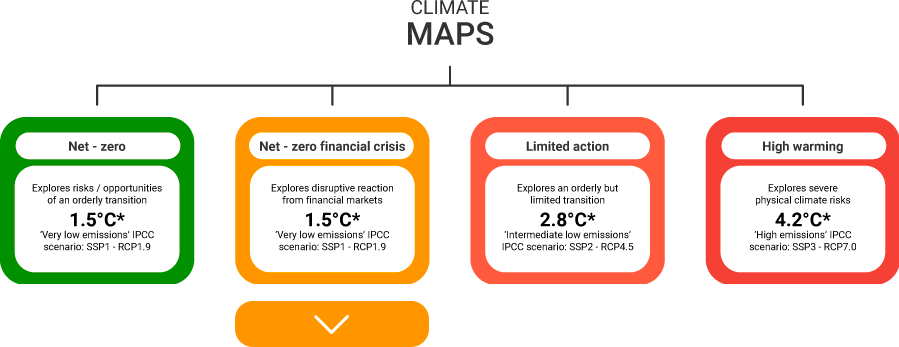

Ortec Finance uses four key scenarios to project the expected socioeconomic global changes due to climate change (including transition and physical risks). These scenarios are based on the five shared socio-economic pathways previously used in the IPCC Sixth Assessment report. They differ in terms of responses in policy and technological changes, physical risks, and pricing-in mechanisms. They result in the below four key climate scenarios:

The climate scenario OIM sustained to design the optimal asset allocation for the fund is the “Net-Zero Financial Crisis”. This scenario strives for global carbon neutrality by 2050 and is aligned with a 1.5°C average temperature increase by 2100. It assumes sudden divestments to align portfolios to the Paris Agreement goals have disruptive effects on financial markets with abrupt repricing followed by stranded assets and a sentiment shock.

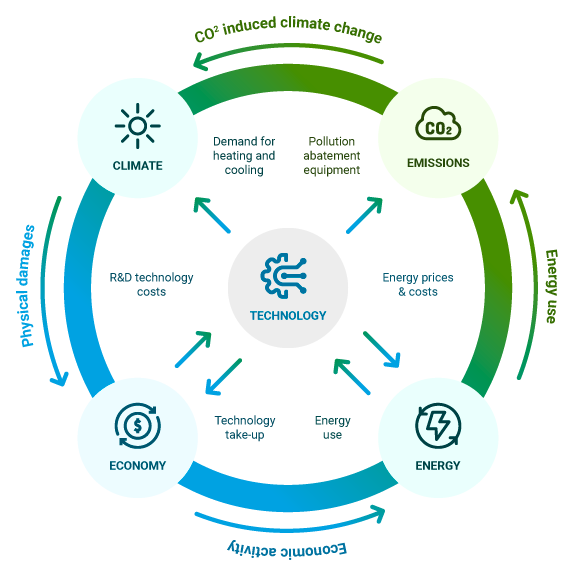

These scenario assumptions are then integrated into a macroeconomic model: they drive macro-economic changes per region and sector. The economic impacts from the above climate change-related drivers are estimated using an econometrics model that considers interactions between the environment, energy, and the economy. Ortec Finance uses then a stochastic financial model to define climate systemic risk through climate change-adjusted economic and financial outlooks for a 40-year horizon, as well as climate impacts on asset return projection per asset class, country and sector.

Source: Ortec Finance

Relative to the Ortec Finance Scenarios (OFS), the NZFC scenario is mainly characterised by lower returns and higher inflation levels. When running optimisations, the distribution of allocations across the optimal portfolios for the NZFC scenario shows clear differences with the OFS. Nearly all portfolios allocate substantially more to fixed income products, while the allocation to public equities is comparably small. The latter is driven by the unfavourable equity return expectation, especially for the first 10-years as financial markets are disrupted by sudden divestments. The exposure to real assets, ends up being similar or smaller in size than under the OFS and positive scenario. More differences could be observed within these three main groups, at the asset class level.

Ortec Finance Scenarios (OFS)

Baseline - neutral scenario

Moderate growth outlook

Risk premia lower than historical average

Rates remain higher than past 2 decades

Net Zero Financial Crisis (NZFC)

Negative scenario

Sudden divestments to align portfolios to the Paris Agreement goals (net zero 2050 - 2070) have disruptive effects on financial markets with abrupt repricing in the period 2025 - 2030 followed by stranded assets and a sentiment shock

Growth picking up

Positive scenario (OPS)

A more optimistic outlook

Energy prices drop, causing a steep reduction in inflation

This will improve purchasing power of households, and allows central banks to cut rates, which will restart global growth in 2024

Figure 4 - Ortec Finance's stochastic scenarios used for optimization (Ortec Finance, 2023)

The conclusions of the optimisations were combined with sensitivity analyses and qualitative considerations. This resulted in two portfolios being recommended.

In its analysis, Ortec Finance also runs climate change stress tests and compares the performance of the two recommended portfolios to the current SAA under various climate scenarios.

Although it is impossible to predict which scenario would unfold, let alone its financial impact, these climate scenario-driven stress tests provide valuable information into the risks faced by OIM and the robustness of the current and proposed strategies under various economic and financial market conditions. The main purpose of this analysis is to assess that the proposed portfolios do not deteriorate results under various potential climate scenarios.

Ortec Finance found that both proposed portfolios outperform the current SAA in all the analysed climate risk scenarios.